市场资讯及洞察

.jpg)

一、罕见的"4票反对":分裂房间里的最后一课

2026年4月29日,鲍威尔主持了他作为主席的最后一次FOMC会议。会议决议本身并不意外——联邦基金利率目标区间维持在3.5%—3.75%,符合市场近100%的预期。但真正震动市场的,是会议投票结果:8票赞成、4票反对,创下自1992年10月以来反对票数量最多的纪录。

这4张反对票呈现出戏剧性的"双向分裂"。被视为特朗普代言人的理事米兰投反对票,主张立即降息25个基点;而克利夫兰联储主席贝丝·哈马克、明尼阿波利斯联储主席尼尔·卡什卡里和达拉斯联储主席洛里·洛根则站在另一端,反对在声明中保留宽松倾向措辞。有财经记者尖锐地指出,本次决议暴露的不仅是政策分歧,更是美联储内部对未来路径的根本性分歧。

更具历史意义的是,鲍威尔在新闻发布会末尾留下了那句意味深长的告别——"非常感谢大家,下次不再见。"5月15日,他的主席任期将正式结束,由特朗普提名的凯文·沃什接任。但鲍威尔宣布将继续留任理事,"任期时长待定",此举将使继任者沃什的政策推进面临更复杂的委员会票数博弈。

二、PCE数据爆表:通胀回归"3字头"的警报

会议次日公布的PCE数据为美联储的鹰派立场提供了支撑,也将其困境暴露无遗。

3月PCE物价指数同比从2月的2.8%大幅跃升至3.5%;剔除食品和能源后的核心PCE通胀率从3.0%上升至3.2%——这是自2023年11月以来的最高水平。从1月核心PCE的3.1%,到3月的3.2%,再叠加整体PCE的3.5%,美联储2%的通胀目标已经渐行渐远。

通胀压力的来源结构正在发生根本性变化。一方面是2025年4月以来关税政策的滞后效应持续渗透至商品价格;另一方面,更直接的冲击来自2月底美国和以色列对伊朗发动军事行动后的能源价格飙升——汽油平均价格上涨约44%,WTI原油结算价单日大涨6.95%至106.88美元/桶,布伦特原油升至118.03美元/桶。鲍威尔在新闻发布会上承认,"高企的油价将在短期内推高整体通胀",并坦言美联储正在研究"关税只产生一次性价格影响"的假设。

三、GDP的"虚强实弱":增长引擎的结构性隐忧

与通胀数据同日公布的Q1GDP数据则呈现出"虚强实弱"的特征。第一季度实际GDP年化增长2%,较2025年Q4政府停摆拖累下的0.5%大幅反弹,但仍低于市场普遍预期的2.2%—2.3%。

拆解GDP构成可见三大特征:第一,消费支出增长1.6%,较Q4的1.9%继续放缓,反映出油价飙升和密歇根大学消费者信心指数跌至历史最低点的影响;第二,出口增长近13%(几乎全部由货物运输驱动),延续了2025年以来"抢出口"扭曲常态化的特征;第三,最值得关注的是非住宅固定投资增长10.4%,知识产权和设备支出尤为强劲——这背后是AI数据中心建设的"无止境需求"。鲍威尔在记者会上特别强调:"全美各地对数据中心的需求似乎永无止境"。

但这种"AI驱动+净出口扭曲+消费降温"的增长结构存在脆弱性。一旦AI投资周期出现拐点(如英特尔大跌17%所暗示的),或地缘冲突进一步升级压制消费,增长引擎可能快速失速。

四、政策路径:滞胀逻辑下的降息门槛抬升

综合三组信号——分裂的美联储、3.2%的核心PCE、2%的GDP增速——可以勾勒出货币政策的新框架:美联储正从"何时降息"的讨论,转向"是加息还是降息"。

对市场而言,这意味着三重压力:美元指数重回100上方对非美资产构成压制;美债收益率高位震荡延长"高利率长周期";风险资产的估值锚正在重新校准。

五、大类资产展望:股市、黄金、数字货币的三种命运

股市:AI叙事支撑下的"高位结构市"。 标普500、纳指在4月中旬连创新高,纳指100一度录得12连涨,但本次议息会议后美股反应分化——道指连续5个交易日下跌,标普微跌、纳指微涨,英伟达、微软等科技龙头跌超1%。这种分化揭示了市场的真实状态:AI数据中心建设的"永无止境需求"仍是核心引擎,但高利率环境下估值容忍度下降,叠加四大科技巨头财报的"AI验证时刻",资金正从无差别上涨转向严苛的业绩兑现筛选。

黄金:长期牛市未变,短期需警惕"滞胀对冲"与"获利了结"的拉锯。多空逻辑非常清晰:多头逻辑——核心PCE回到3.2%、地缘冲突未解、各国央行持续购金、美元信用受质疑;空头逻辑——美联储降息预期持续推迟、实际利率维持高位、黄金ETF高位出现净流出。机构展望分歧明显:高盛预测年底4900美元,摩根大通看到5055美元并维持2028年6000美元长期目标,但麦格理保守预测2026年均价仅4323美元。对普通投资者而言,黄金作为"滞胀对冲+央行去美元化"的中长期配置逻辑依然成立。

六、结语:货币政策的"历史性十字路口"

鲍威尔八年任期落幕,留下的是一份功过交织的账单——月均失业率4.6%创历史佳绩,但任内平均通胀3.09%远超2%目标。他的继任者沃什将接手一个更为复杂的局面:通胀粘性、地缘冲突、增长结构性脆弱、委员会内部的撕裂。在这个"供给冲击常态化"的新世界里,传统的需求管理框架正面临深刻挑战,资产配置的核心命题已从"押注降息节奏"转向"在滞胀阴影下寻找现金流和稀缺性"——这或许是鲍威尔留给市场最深刻的启示。

XAUUSD Analysis 10 – 14 April 2023 The gold price outlook is positive in the medium term. As last week's closing of the buying bar was above the 1960 support or the latest high in price on the Weekly timeframe, it indicates continued buying momentum that will allow the price of gold to recover. It can rise further to test the 2070 resistance level, which is a key resistance at the weekly time frame level or the price level that gold has ever hit the most in history.

But even so, the price of gold remains negative in the short term. There may be a fall to adjust the consolidation or sideways around the 1985 and 1976 support, which are important support levels in the H4 and H1 timeframes that are worth watching. because if the price cannot go down deeper than the above two support levels The direction of gold prices is likely to continue to rise. Corresponds to the large timeframe in the medium term where the price is Up Trend.

And in the event that the price of gold cannot continue to rise, but there is a breakout of the 1985 and 1976 support levels, it can come down with continuous selling pressure. Daytime support at the 1960 price level or the latest price high in the Weekly timeframe are the next targets to watch. AUDUSD Analysis 10 – 14 April 2023 AUDNZD price bears a negative view on the short and medium term.

Due to the continuous decline in the Weekly timeframe, the price is likely to bear down and can continue to fall. After the price has corrected sideways on the Daily timeframe, when looking at the H4 timeframe, a sharp swing of the price can be seen, which is a sideways movement between support 1.06730 and resistance 1.07930. Rara then broke out the support 1.06730 down with a sell candlestick with more momentum than a buy candlestick.

Therefore, it can be expected that Price may continue to decline to retest the support 1.04690 or the previous Low on the Weekly timeframe. GBPUSD Analysis 10 – 14 April 2023 The GBPUSD trend is currently rallying to test the 1.24470 resistance with continued buying momentum as seen by the weekly timeframe buying pressure candlestick, although last week's closing price was truncated. Any intestine dumper Still, the price has yet to show a strong sell candle on the Weekly timeframe, indicating a clear uptrend in both the short and medium term.

Forecasting that price, there is a tendency for the price to correct sideways at the 1.24470 resistance area before rising to test the next resistance at 1.26660 on the daily timeframe level, where the key support is 1.22700, which is the time level support. The H4 frame predicts that the price may retrace to test. If the price cannot stand on the resistance of 1.24470 and continue to rise

热门话题没错,特斯拉又降价了!马斯克在4月8日针对特斯拉降价发表回应,降价的原因不是大家对特斯拉没有需求,而是大家没钱负担不起,只有把车价降下来,才是真正的满足需求。“许多富裕的批评家不明白大规模需求受到负担能力的限制。我们的产品有很多需求,但如果价格比人们拥有的钱多,那么这种需求就无关紧要了。”

在宏图3并没有发布特斯拉新车型令人失望后,特斯拉股价也一直难以站稳200美金之上,目前可以给市场交代的,也就是不断降价和推出廉价款,让特斯拉更加亲民。而随着特斯拉破纪录的交付量,车辆销售不能脱节,降价促销也是大势所趋。据特斯拉美国消息,其已将长续航版和高性能版Model 3在美国的起售价降低了1000美元,售价分别为41990美元和52990美元。此外,特斯拉正式在美国推出了一款价格较低的新型Model Y,配备AWD动力系统,售价仅为49990美元。现有的两款Model Y价格也下调了2000美元,Model Y LR由54990美元下调至52990美元,Model Y P价格由58990美元下调至56990美元。根据美国国税局(IRS)最新指导意见,自4月18日起后轮驱动版Model 3的7500美元联邦税收抵免将削减至3750美元。整体来说客户口袋里掏出去的钱还是没有降低,反而是政府补助降低了不少,因此特斯拉降价大趋势还将延续,否则正如马斯克所说,很多有需求但买不起车的客户会慢慢被竞争对手抢走。本次特斯拉美国市场的降价也是今年以来的第三次降价,前两次分别发生在1月和3月,经历三次降价后,Model S从2022年底的104990美元降至84990美元,上面提及的Model Y和Model 3都在持续降价中。这点我们从马斯克在去年第四季度财报会议上就可以得到验证,特斯拉下一代车型的尺寸将小于目前在售的Model 3和Model Y,成本将是现有平台的一半。今年3月,特斯拉总工程师Lars Moravy也表示公司希望以目前Model 3或Model Y一半的成本制造下一代汽车。在今年年初,马斯克在电话会议中回应特斯拉降价时就表示,很多人都想买一部特斯拉电车,但是可能负担不起,所以我们在市场上的价格调整也将迎合普通消费者的需求。特斯拉发布的最新数据显示,2023年一季度特斯拉在全球累计生产电动车约44.08万辆,同比增长44.3%,累计交付新车约42.29万辆,同比增长36%,打破了特斯拉单季度的交付纪录。如果特斯拉推出价格更低、级别更小的车型,将对欧洲、日本等更青睐小型电动车的市场形成有效占领。届时该低价小车型或为特斯拉带来远超Model 3的全球交付规模,特斯拉的战略转变也将帮助其迅速占领新能源车市场,特别是欧美国家在代替化石燃料车进程中所需要的清洁能源车。不断降价的特斯拉也变得更加亲民,随着不同车型针对不同消费阶层而定向推出,特斯拉在新能源电车领域的老大地位将变得更难动摇。免责声明:GO Markets分析师或外部发言人提供的信息基于其独立分析或个人经验。所表达的观点或交易风格仅代表其个人;并不代表GO Markets的观点或立场。联系方式:墨尔本 03 8658 0603悉尼 02 9188 0418中国地区(中文) 400 120 8537中国地区(英文) +248 4 671 903作者:Xavier Zhang | GO Markets 专业分析师

免责声明:文章来自 GO Markets 分析师和参与者,基于他们的独立分析或个人经验。表达的观点、意见或交易风格仅代表作者个人,不代表 GO Markets 立场。建议,(如有),具有“普遍”性,并非基于您的个人目标、财务状况或需求。在根据建议采取行动之前,请考虑该建议(如有)对您的目标、财务状况和需求的适用程度。如果建议与购买特定金融产品有关,您应该在做出任何决定之前了解并考虑该产品的产品披露声明 (PDS) 和金融服务指南 (FSG)。

免责声明:文章来自 GO Markets 分析师和参与者,基于他们的独立分析或个人经验。表达的观点、意见或交易风格仅代表作者个人,不代表 GO Markets 立场。建议,(如有),具有“普遍”性,并非基于您的个人目标、财务状况或需求。在根据建议采取行动之前,请考虑该建议(如有)对您的目标、财务状况和需求的适用程度。如果建议与购买特定金融产品有关,您应该在做出任何决定之前了解并考虑该产品的产品披露声明 (PDS) 和金融服务指南 (FSG)。

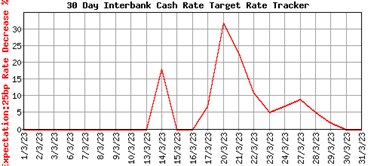

热门话题4月4日澳洲东部时间下午2:30分,澳联储宣布维持现有利率3.6%不变,暂停加息。是美国及瑞士银行业危机以来首个暂停加息的主要国家央行。

决议公布前ASX利率预期回顾根据ASX利率预期追踪,3月对于降息25bp的预期一度超过30%。而在美联储3月31日公布加息25bp后,降息预期为0%,暂停加息为100%。因此本次暂停加息符合市场预期。

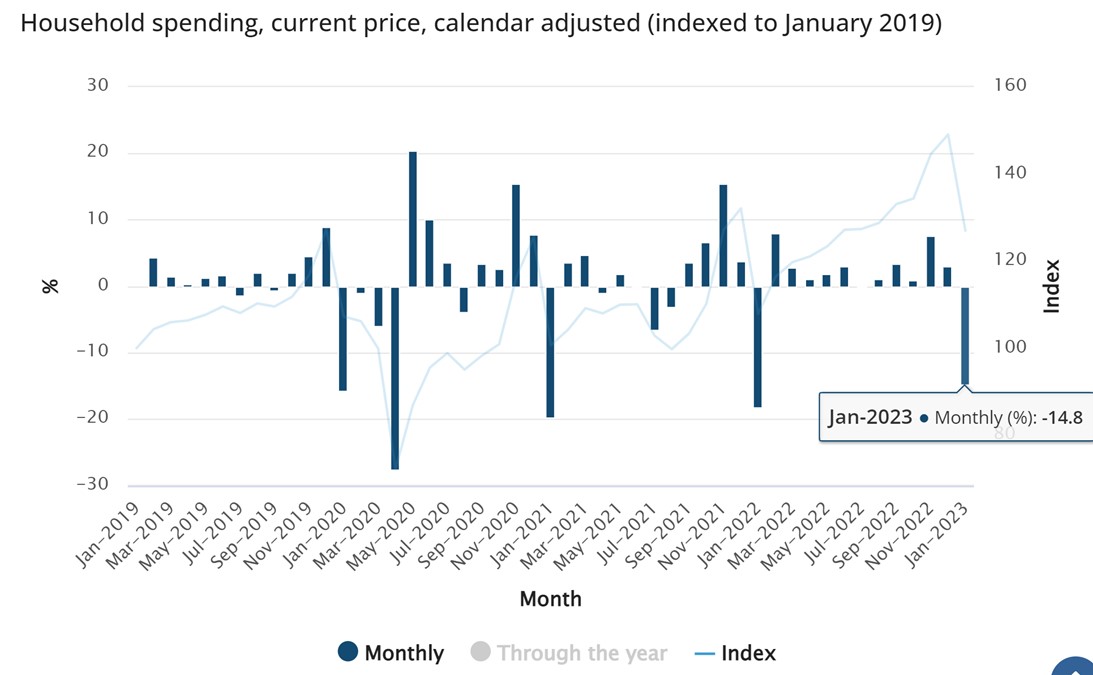

近一年来在连续10次加息后,澳大利亚的官方利率已经从疫情紧急情况时的0.1%上升了350bp到3.6%。今天的决议虽然意味着澳大利亚央行的现金利率将保持在3.6%,但注意这仍是2012年5月以来的最高水平。本次加息声明中强调本月的利率按兵不动是由于货币政策的影响对经济存在滞后性,因此目前澳联储正等待更多有效数据以提供下一步决策的支撑。与前几次声明措辞相比,本次强调了在美国及瑞士银行风波下澳洲银行系统的强健及稳定性,并且指出在高息环境以及物价压力下居民支出已经呈现放缓趋势。我们认为这也算是对近期澳洲人民怨声载道的浮动利率贷款的一个回应,暂停加息给房屋贷款者一丝喘息机会。三大关注点:通胀、支出、就业通胀数据方面,澳洲每月消费者物价指数(月度CPI)连续两个月下降,3月28日公布的2月月度CPI显示,从12月的8.4%,到1月的7.4%,再到2月最新的6.8%,也是支撑澳联储本次温和决议的关键。注意,2022年不停攀升的季度CPI是澳联储前期加息的主要依据,2022年4季度同比增速7.8%,其中尤其以服务业通胀增速居高不下,已接近08年以来峰值5.5%。而关键数据季度CPI数据一般于上季度结束后的一个月公布,即,4月26日即将公布2023年1季度CPI关键数据。因此这可能也是澳联储按兵不动的另一主要原因,5月利率决议会更加明朗化。支出方面。澳大利亚2月零售销售持续疲软,2月零售销售环比仅增长0.2%。3月14日公布的家庭支出数据出现明显的下降,2023年1月同比大幅下降14.8%。进一步证明在澳联储加息下,面对不断上升的借贷成本,消费者开始采取紧缩措施,这支持了澳洲联储按兵不动的理由,消费的弹性一直是政策制定者对经济能够承受加息抱有信心的关键因素。

劳动市场数据保持强劲,失业率仍在历史低位3.5%。澳洲经济学家指出,海外移民带来的人口增长加快的预期可能会快速弥补目前已经见顶的岗位空缺,就业有可能进一步放缓。3月30日公布的2月职位空缺季度调整数据自21年8月以来首次下跌1.5%。澳联储一直对加息环境下引发的物价/薪资螺旋效应尤为警惕。因此后续该数据也是决定加息进程的关键因素之一。暂停加息,而非不加息,何时降息澳联储进一步提示在全球通胀环境下货币政策是必要的且会继续实施相关货币政策以确保通胀回落到目标区间。根据市场普遍预期,在5月到6月至少还会继续加息一次。根据最新的四大行预测,澳新银行预测4月和5月均会加息,利率峰值为4.1%并保持到2024年11月。其余三家行预测最快2024年初开始削减利率。

Westpac西太银行下调利率峰值预期,从原有的4.1%到目前的3.85%。4月暂停,5月加息25bp。利率将从明年第二季度的3月至5月开始再次下调,而到明年年底,利率将下降至2.85%。CBA联邦银行也支持这样的预测,即5月份利率只会再加息一次,峰值达到3.85%。由于经济放缓、失业率攀升和价格压力缓解,利率最早将于11月下调。到2024年年中,利率将下滑至2.85%。NAB国民银行对 2024 年更大幅度的降息并不乐观。那么澳洲加息何时结束?首先看澳洲的通胀情况,目前月度数据已经有所缓和,等待后续关键数据释放。而最重要的就是关注全球尤其是美国加息周期的结束。什么时候美联储决定结束,那就是我们应该期待的终点。根据CME美联储利率观察工具最新显示,市场预计美联储5月份继续加息25个基点的可能性为54.3%,可能受周一原油价格的飙升影响较上周五48.4%有所回升,但是这种几率的增加不会改变美联储政策前景已经大体转向鸽派的趋势,所以我们看到美元指数周一冲高后最终回落。记住,澳联储始终强调寻求“软着陆”而不是将澳大利亚推入衰退,因此叠加美国及澳洲预期均转鸽,终点可能并不遥远。相关投资产品表现消息公布后,澳元对美元下跌超过30个基点,当日最低至0.6720美元,但是下方0.6565处有强劲支撑,多头仍可等待性价比高的的盈亏比点位。ASX200指数本身一方面已消化暂停加息预期且担忧澳联储后续加息,冲高0.26%后回落表现疲软当日最终收跌0.01%,终结一季度未的7连涨。另外一方面,昨日公布的美国JOLTS职位空缺数据不佳,对经济衰退的担忧可能蔓延。免责声明:GO Markets分析师或外部发言人提供的信息基于其独立分析或个人经验。所表达的观点或交易风格仅代表其个人;并不代表GO Markets的观点或立场。联系方式:墨尔本 03 8658 0603悉尼 02 9188 0418中国地区(中文) 400 120 8537中国地区(英文) +248 4 671 903作者:Cecilia Chen | GO Markets 分析师

Equity markets US markets dipped last night with the Dow finishing down for the first time in 4 sessions. This came as the streak of better-than-expected economic data came to an end with initial jobless claims unexpectedly jumping to a one-month high last week. Retail giant and Dow 30 component Walmart (WMT) also weighed on the index dropping 6.5 per cent after it missed quarterly profit estimates and predicted a low-single digit rise in fiscal 2022 net sales.

Source: Yahoo Finance Whilst US Markets are flat for the week, UK and Asian equity markets have performed well with signs of China's economic recovery continuing lifting the Hang Seng and good news on UK vaccination progress sending the FTSE 100 higher. Source: Bloomberg The ASX200 again hit post COVID highs this week before pulling back slightly. Optimism in the Australian economic recovery was bolstered this week with another drop in the unemployment rate and vaccine rollouts imminent.

Forex markets FX markets were mixed this week, the US dollar strengthened modestly against most major currencies, with the exceptions of CAD, AUD and GBP. Source: Bloomberg Resource linked currencies AUD and CAD performed well as prices for Copper and Iron ore continued to run hot, with increased demand from China and ongoing COVID related supply issues underpinning the price of these resources. Source: marketindex.com.au GBP outperformed this week amid continued optimism over the nation’s vaccine rollout, with the pound touching the highest level versus the euro since March last year.

Source: GO MT4 Commodities Gold Spot gold (XAUUSD) continued its downtrend setting a new low price for 2021 and within touching distance of the lows set in November. With markets risk on as vaccines rollout and positive signs of an global economic recovery the lustre has been taken off the precious metal for now. Source: GO MT4 Oil US crude prices broke above $60 per barrel touching as high as $62, a level not seen since January 2020.

Severe winter storms and rolling blackouts in the oil producing state of Texas have crippled the oil industry, causing an output drop of more than 4 million barrels a day - almost 40% of the nation’s crude production. Monday, 22 February 2021 Indicative Index Dividends Dividends are in Points ASX200 WS30 US500 US2000 NDX100 CAC40 STOXX50 0.821 6.645 0.323 0.011 0 0 0 ESP35 ITA40 FTSE100 DAX30 HK50 JP225 INDIA50 0 0 0 0 0 0 10.131

We had an eventful week on global markets with the inauguration of a new US administration and a dovish stance from the European Central bank fuelling hopes of extended fiscal stimulus in the new year. Equity markets Risk appetite got a boost this week from a push by US authorities for nearly $2 trillion in additional spending and plans to jumpstart a federal response to the COVID pandemic. US equity markets had the best post inauguration performance since the 1980’s driving the S&P 500, Dow Jones and NASDAQ indices to record highs.

The NASDAQ was also helped along by big beats from Netflix and Intel who reported earnings this week. With this lead Australia's share market hit 11-month highs, with help from an improved unemployment rate supporting investor optimism. European markets also performed well after ECB’s decision to reconfirm its very accommodative monetary policy last night.

Source: Twitter COVID With Executive Orders from the new US administration seeking to accelerate the rollout of vaccines and the seeming peak in US COVID cases there was optimism this week from major Wall St analysts that we could be seeing “the beginning of the end of the COVID crisis" in the US. Goldman's top economist Jan Hatzius, writes that "a vaccine-driven reduction in hospitalizations is likely to kick off the growth rebound through relaxed restrictions and some reductions involuntary consumer social distancing." Source: Zerohedge Forex market While record planned US stimulus helped push equities higher it also created a headwind for the US Dollar which continued its downtrend. All major currencies performed strongly against the greenback this week.

Source: Bloomberg Aussie Dollar AUDUSD strengthened this week driven by US dollar weakness and a better than expected unemployment rate of 6.6% indicating continued recovery of the Australian economy from the COVID economic shock. AUD is trading in a tight range and has managed to hold the important 0.77c support level. Gold Spot gold (XAUUSD) had a strong week on the back of US dollar weakness and stimulus hopes, it bounced strongly from the 1820 -1800 support zone making 2 week highs and being up around 2% for the week at time of writing.

Negotiations in the US on the particulars of the proposed stimulus bill and positive or negative news on regarding COVID are expected to play a part in the next few weeks of future price movements. Source: GO MT4 Cryptocurrencies It was a tough week for Cryptos with flag bearing tokens Bitcoin and Ethereum among others sliding dramatically after recent stellar rallies. Bitcoin dropped 10% alone on Thursday and down almost 20% on the week.

The drop seems to be a long overdue correction and sustained profit taking, it wasn’t helped on Thursday by a report in a trade blog suggesting that there had been what’s known as a double purchase, where the same “coin” is used in two separate transactions. This rumour went viral casting doubt on the security of the Bitcoin blockchain. Industry veterans and people familiar with blockchain technology downplayed the notion, but with so many new investors with a poor understanding of blockchain technology the damage was done.

From a chart technician's point of view, Bitcoin broke the lower barrier of the wedge pattern it has been consolidating in and has headed to the important 30000 support level. Source: GO MT4 Monday, 25 January 2021 Indicative Index Dividends Dividends are in Points ASX200 WS30 US500 US2000 NDX100 CAC40 STOXX50 0 0 0 0.012 0 0 0 ESP35 ITA40 FTSE100 DAX30 HK50 JP225 INDIA50 0 0 0 0 0 0 0

Equity markets US markets dropped sharply overnight as inflation fears returned on the back of Treasury yields hitting their highest levels in more than a year. Investors are concerned the Federal Reserve will allow inflation to accelerate, after Wednesday’s policy meeting where they reaffirmed their commitment to easy money policies. As seen previously the hardest hit stocks were the growth small caps and Tech companies on the Russell and NASDAQ, as traders rotated out of these sectors into traditional value stocks tracked by the Dow Jones index.

The Dow did touch all time highs during the session before fading in the afternoon. Dow Jones down 153 (0.46%) NASDAQ down 409 (3.02%) S&P 500 down 58 (1.48%) Russell 2000 down 69 (2.94%) Source: Yahoo Finance The Australian equity market had a choppy week, mirroring its US counterparts as economic enthusiasm battled with fears of rising interest rates. The ASX 200 dropped yesterday with the sell-off continuing today as much better than forecast employment figures saw market expectations of rising interest rates coming sooner than previously expected.

Source: Yahoo Finance World equity indices are mostly flat for the week as markets see sawed between all time highs and steep declines. Evidence of rotation from Growth and momentum stocks into traditional value stocks in the US is evident from Dow's outperformance of the NASDAQ and S&P 500. The ASX 200 also dropped over the week as rising Aussie and US bond yields plus a strong employment report had investors reassessing predictions of when the RBA would start a tightening cycle on rates.

Source: Bloomberg Forex markets FX markets saw a mostly stronger US dollar against most major currencies. Rising bond yields in the US have mostly driven this move higher - higher interest rates make the US dollar a more attractive investment than its counterparts. Traditional safe haven currencies the Swiss Franc and Japanese Yen were the only major currencies to outperform the US dollar this week, on a choppy performance in equity markets.

Source: Bloomberg Commodities Gold Spot gold (XAUUSD) was the other safe haven that rallied against the US dollar, being modestly up for the week at the time of writing. Despite a mostly rising US Dollar, gold ground higher on inflation fears spurred by rising rates in bond yields. Source: GO MT4 Oil US crude prices dropped sharply this week as US crude found stiff resistance around the $67 a barrel price level after a recent strong run up.

US Crude plunged more than 9% in yesterday’s session at one point, on concerns new COVID lockdowns in Europe will sap demand, and whether the recent run up is justified with the current progress of world economic recovery. Source: GO MT4 Bitcoin Bitcoin gapped on the Monday open to set a record price above $60k US per token. This after an extremely volatile week which saw the cryptocurrency ranging from 53k – 60k Whether the cryptocurrency has run out of steam at these levels or is preparing for another push higher remains to be seen.

Source: GO MT4 Monday, 22 March 2021 Indicative Index Dividends Dividends are in Points ASX200 WS30 US500 US2000 NDX100 CAC40 STOXX50 0.081 0 0.01 0.024 0 0.098 0 ESP35 ITA40 FTSE100 DAX30 HK50 JP225 INDIA50 0 1.454 0 0 0 0 1.072