市场资讯及洞察

5 月伊始,联邦基金目标利率区间维持在 3.50% 至 3.75%。美联储刚刚结束了 4 月 28-29 日的议息会议,投资者正进入一个政策真空期,直至 6 月 16-17 日的下一次决议。然而,地缘政治背景远非平静。由于伊朗冲突导致霍尔木兹海峡处于事实上的关闭状态,布伦特原油价格已飙升至每桶 108 美元附近,国际能源署将其描述为“史上最大的能源供应冲击”。

本月的宏观矛盾既直接又令人不安:由能源驱动的通胀脉冲,正撞上 3 月份表现意外强劲的劳动力市场,而第一季度的增长数据却依然疲软。这种带有“滞胀”色彩的组合拳,直接挑战了美联储目前的政策路径。

美联储此前已将 2026 年 PCE 通胀预期上调至 2.7%,并继续暗示年内仅有一次降息,尽管市场对具体的降息时点仍持有异议。由于 5 月没有 FOMC 议息会议,每一项重磅数据的发布都将比往常承载更多的权重,成为投资者博弈 6 月政策走向的关键筹码。

经济增长:业务活动与需求

步入 5 月,经济增长的前景表现不一。第一季度 GDP 初步预览值已于 4 月 30 日公布,而此前疲软的零售销售和库存数据,使得整体需求端的局势变得更加难以捉摸。

ISM 制造业指数一直是乐观情绪的一个低调来源,近期的数值始终维持在扩张区间。然而,逆风的来源正在发生变化:能源成本和关税效应目前是决定业务活动下一步走向的最关键变量。对于那些已经在应对高昂投入成本的企业来说,108 美元的油价与贸易摩擦的结合,将是对企业韧性的一次重大考验。

劳动力:非农与就业数据

4 月的就业形势报告是本月最集中的风险事件之一。尽管 3 月非农数据强于预期,但此前的修正值使得整体趋势显得有些模糊。4 月的数据将起到决定性作用:揭示劳动力市场是在高利率背景下真正实现了“再加速”,还是仅仅在消化季节性噪音。

通胀:CPI、PPI 与 PCE

4 月的通胀数据是本月对市场影响最大的板块。3 月消费者价格指数 (CPI) 同比上涨 3.3%,其中能源成本月度上涨 10.9%,汽油价格飙升 21.2%,贡献了整体涨幅的近四分之三。鉴于布伦特原油在 4 月下旬维持在 105 至 108 美元之间,能源成本进一步传导至 4 月 CPI 几乎已成定局。尽管整体通胀数据引人注目,但核心 CPI 和核心 PCE 依然是研判美联储底层通胀趋势的关键指标。

政策、贸易与企业盈利

由于 5 月没有 FOMC 议息会议,政策关注点将转向美联储官员的讲话以及备受瞩目的领导层更迭。美联储主席杰罗姆·鲍威尔的任期将于本月中旬结束。唐纳德·特朗普总统已提名 凯文·沃什 (Kevin Warsh) 为下一任主席,市场正密切分析其听证会内容,以寻找央行独立性或政策倾向是否会发生转向的蛛丝马迹。

在地缘政治方面,已进入第九周的伊朗冲突仍是最大的宏观尾部风险。霍尔木兹海峡的封锁和停滞不前的美伊谈判为能源价格设定了较高的底部支撑。同时,第一季度财报季进入高峰期,预计 5 月 7 日将是报表发布最密集的一天,市场将重点关注零售和周期性行业如何应对利润率的挤压。

本月核心监控清单

- 美伊谈判: 关注霍尔木兹海峡运行状态的任何进展。

- 美联储语调: 官员在会议间隙期辞令的任何细微转变。

- 盈利质量: 尤其是零售、能源及周期性行业的表现。

- EIA 原油库存: 通过周度数据衡量国内供应缓冲情况。

- 关税公告: 任何可能推高通胀预期的贸易摩擦信号。

核心总结 (Bottom Line)

绝不能因为 5 月没有议息会议就认为这是一个平淡的月份。在 6 月决议之前,非农、CPI、PPI 和 PCE 数据将悉数出炉,而原油依然是主要的外源性冲击。对于市场而言,核心问题在于:我们面对的是一次暂时的能源驱动型通胀上升,还是在增长放缓的同时出现了一个更广泛的系统性通胀问题?这一区别将决定债券、美元、黄金及股指的下一个大级别走势。

The week kicked off with a series of ECB speeches, and markets participants were gearing up to have more updates on the Eurozone economy, interest rate and Italy. Investors were keen to see whether the ECB downplays the slowdown in the German economy and the Italian Budget risks. We bring you a summary of the main headlines following the speeches: ECB’s Praet Speech: Peter Praet is a member of the ECB’s Executive Board since 2011.

The most captivating headlines from the latter are probably: “ The eurozone has lost some growth momentum, and headwinds are becoming increasingly noticeable.” He also argued that there is limited spillover from Italy so far. Praet acknowledged how the factors related to protectionism, financial market volatility and vulnerabilities in emerging markets are creating headwinds. He reiterated that the ECB policy will remain predictable and will proceed at a gradual pace.

He mentioned that it would need a big change in scenarios not to abide by rate guidance. ECB’s Nowotny Speech: Ewald Nowotny is the governor of the National Bank of Austria and member of the European Central Bank (ECB)’s governing council. Nowotny discussed the quantitative easing program and that the ending process poses little risk to financial stability.

He believes that “ a well-communicated exit may benefit financial health and very low rates for a long time may impair stability ”. ECB’s Coeuré Speech: Benoît Cœuré is a member of the ECB's Executive Board. The speech was mainly focused on Growth, Europe and Togetherness.

His speech captures how to reap the benefits of the Single Market. He highlighted how Europe’s East is not catching up which might question the value of the EU. “There have been some notable improvements in certain countries over time, but in others the process of gradually catching up with their EU peers appears to have stalled, or even to have backtracked, in recent years.” “And if there is no credible prospect of lower-income countries catching up soon, there is a risk that people living in those countries begin questioning the very benefits of membership of the EU or the currency union.” ECB’s President Draghi’s Speech: The President provided further insights into the euro area outlook and the ECB’s monetary policy. “The data that have become available since my last visit in September have been somewhat weaker than expected.” “A gradual slowdown is normal as expansions mature and growth converges towards its long-run potential…. Some of the slowdowns may also be temporary.” “Underlying drivers of domestic demand remain in place.” Overall, he expressed that the ECB maintained their view that the economy was still in line with expectations.

However, inflationary pressures were lower than expected which means that while bond purchases are set to end in December, the ECB will maintain significant monetary stimulus due to the moderation in recent data.

Dissecting the FOMC Statement The US Federal Reserve cut interest rates overnight by 25 basis points, taking the US Federal Funds rate to 2.25%. The rate cut was mostly seen as a hawkish one. In the press conference, Chair Powell said that the central bank’s rate cut was a “mid-cycle adjustment to policy ” rather than “the beginning of a long series of rate cuts.” We have dissected the July FOMC statement in comparison with the June statement to highlight the changes for ease of reference.

Deutsche Bank Revives The Failure of Lehman Brothers Deutsche Bank’s woes dominated headlines this week. On Sunday, the multinational investment bank announced 18,000 job cuts around the globe by 2022 and shut down its global stock trading business as part of a sweeping overhaul. It was reported that the cuts had been anticipated for weeks.

We watched the staff of the German bank being laid off around the world including, Sydney, New York, and London offices this week. It was difficult to witness the lay-offs of the troubled bank without reviving the moments of Lehman Brothers. Since the 2008 financial crisis, the bank started its downfall over a series of costly scandals, alleged wrongdoing, and years of mismanagement.

The massive restructuring did little to boost investor sentiment. The market is worried that the overhaul is not enough to deliver shareholders’ value in the future. In the face of its large workforce cuts, there are concerns on the revenue stream from the core European retail and corporate banking.

Additionally, in the era of low global interest rates and an-already struggling European banking sector, Deutsche Bank’s restructuring does not inspire a lot of confidence. Just recently, the Chief Executive Officer, Christian Sewing was celebrating its first major win when Deutsche Bank passed the stress test after it repeatedly failed past exams. The bank’s share price has increased since the beginning of June.

However, this week were the bearer of bad news. The bank might not have anticipated the lack of optimism on the revamp plans. The market has doubts over the restructuring and the ability of the German lender to meet its 2022 profitability goal is highly questionable.

Its share price fell by more than 10% from a high of 8.22 last week to a low of 7.28 this week! Source: Bloomberg Terminal (1 Month Chart) The week got worse as Deutsche Bank is being dragged in a wider probe of a 1MDB scandal. The investigation adds to the list of other high-profile government probes.

The restructuring has not been met with optimism by global rating agencies as well. Now is probably not the time to test the buy the dip strategy.

Critical Hours for Brexit As the clock ticks for Brexit, Brussels and London seem to be working harder than before on their differences for a last-minute Brexit deal. The headlines in the past 48 hours have renewed optimism that the UK and European Union may secure a deal. However, even though the negotiations appear to be moving in the right direction and the related parties are keen to get a deal done, there is still some scepticism on the pace of developments ahead of the EU meeting.

Last- Minute Deal If there are enough concessions to allow for a deal, Prime Minister Boris Johson will have a deal to put through to Parliament in a special sitting on Saturday, the 19 th of October. The circumstances to call for a Saturday meeting are still not clear and are based on how the negotiations unfold. The recent flexibility on both sides is so far paving the way to the UK Prime Minister bringing a deal back from the EU to table in a special meeting on Saturday.

Deal or No Deal The Prime Minister will be forced to ask for a delay - deal or no deal. In the case of a deal this week, it will be a race against time trying to finalise an agreement and arrange for the draft to pass through the votes to exit the European Union on the 31 st of October. But the delay will be mostly to complete the formalities of a deal and will probably not dampen the recent optimism.

In the likelihood, that a deal with the EU is stalled or the deal that the Prime Minister negotiated with the EU is blocked in Parliament, the Prime Minister will be forced to seek for an extension under the Act of Parliament to the Brexit withdrawal data unless he finds a way around the Act. Markets Reactions Brexit hopes have steered risk sentiment in the European markets as the three-year-long Brexit saga seems to be coming to an end. It could be exhaustion that has caused both the EU and UK to be more flexible in allowing Brexit to happen.

European indices rose higher while the FTSE 100 closed slightly in the red due to a resurgent pound. Global equities rallied across the board despite growth forecasts from the IMF. According to the IMF, the global economy is growing at its slowest pace since the financial crisis and would hit only 3% this year.

The UK is expected to grow at 1.2% in 2019 compared to 1.4% last year due to Brexit-related uncertainties. Source: Bloomberg Terminal The British Pound As the UK appears to be on the point of a breakthrough on a Brexit deal, the Pound is soaring and the Sterling has room for more upside movement if Brexit hurdles are cleared. However, in anticipation of more clarity this Wednesday, the GBPUSD pair is in the consolidation phase just below the 1.28 level.

GBPUSD (3 Day-Chart) Source: Bloomberg Terminal We expect the Sterling pairs to remain volatile ahead of the summit! All in all, the path of the Pound in either direction would be sharp and volatile. A deal with the EU backed by parliament could send the pair rallying to 1.40 level while a disruptive no-deal outcome could see the pair plummeting to the lowest level seen in 2016.

热门话题近期AI 人工智能的话题火热,在Chatgpt 4上线后,人们逐渐发现,这一代的AI开始出现了逻辑性甚至是一些的推理性。那么今天就和大家聊一聊AI的摩尔定律和目前发展的情况。

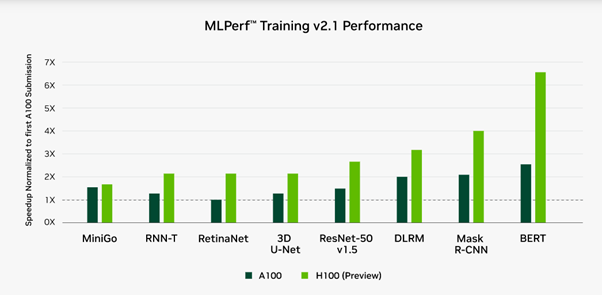

首先和大家简单阐述一下什么是摩尔定律。摩尔定律(Moore's Law)是在1965年由英特尔公司的联合创始人戈登·摩尔提出的观察结果,它预测了半导体集成电路的性能每18到24个月就会翻倍。这一预测在过去几十年中持续成立,使得计算机硬件性能以惊人的速度增长。那么在今年已经开始出现3nm的芯片消息,预计在明年年初将会投入使用,那么对标2020年底的5nm芯片,时间也正好对的上。那么和硬件能力息息相关的AI是不是也会完全遵守摩尔定律呢?这个问题目前来说众说纷纭。比较火热的就是之前OpenAI的 CEO Sam Altman在社交媒体上发布的一段话,AI的摩尔定律将要出现,称全球人工智能运算量每隔18个月翻一番。当然,以个人理性的判断来说,这个具体的数字并不是非常绝对的,因为AI的进步不仅仅只是取决于硬件或者说算力的进步,还是会包括但不限于算法的改进、数据可用性以及计算资源可用性的增加。这些因素都在推动AI的发展,但它们并不受摩尔定律的直接影响。因此,想要描述其AI的进步,可能会考虑的是数据的增长(比如网络数据的指数增长)和算法的改进(比如深度学习等技术的发展)。那么我们由此来简单剖析一下目前的AI训练的情况如何。在前几年,AI的训练还是会花费几天甚至是数周的时间,于是在数十亿的投资之后,各种新兴计算公司接踵而至,包括其中包括Cerebras Systems、Graphcore、Habana Labs以及SambaNova Systems等。此外,Google、Intel、Nvidia等已经建立的公司也进行了类似规模的内部投资。近期新版的MLPerf训练基准测试结果的出炉后,证明了这些投资是很值得的。自从MLPerf基准测试开始以来,AI训练性能的提升“显著超过了摩尔定律”,首先解释下什么是MLPerf。MLPerf是一个行业标准的基准测试,旨在为机器学习(Machine Learning)硬件、软件和服务提供公正、可比较的性能评估。

MLPerf包含了多个任务子类别,从计算机视觉、自然语言处理到推荐系统等,它涵盖了各种常见的机器学习模型和应用场景。MLPerf有两个主要类别的基准测试:训练(Training)和推断(Inference)。MLPerf Training基准测试专注于衡量机器学习模型的训练性能。这包括衡量所需的时间和计算资源来训练一个模型达到预定的质量标准。这个基准测试在多种模型和任务上进行,如图像分类、对象检测、语言模型训练等。说回MLperf测试结果,在之前2021年测试版本中,芯片的迭代和早期对比有两倍的提升。但是软件的改进加上计算器处理架构的进步,速度的提升来到了6-11倍。根据Nvidia的说法,使用A100 GPUs的系统性能在过去的18个月中已经增加了5倍以上,近2.5年增长了近7倍,而在最初的MLPerf基准测试三年前,性能已经增加了20倍。有数据可见,AI的发展速度其实和诸多因素有着关联,然后再近18个月来,其提升速度远超于之前的好几年。

(Source:NVIDIA)在今年年初,英伟达和CEO老黄表示,AI的发展可以克服摩尔定律的逐渐消亡。人工智能的进步可以推动芯片等的性能的提升。老黄解释道:目前的AI行业已经经历了几个重要的发展阶段。第一个阶段是开发人工智能所需的芯片、软件库和系统。这一阶段从2017年之后,发展快到难以想象。第二个阶段包括对感知(如视觉和语音识别)的突破。目前这个阶段已经趋于成熟,感知也开始走向拟人化。目前的阶段是建立智能能力,比如理解世界发生的事情。有逻辑性的推测,对已发生事物的分析和未来的预测。最后一个阶段将是AI软件和现实世界结合起来,用于诸如工厂自动化等事物。日前AI发展的速度远超我们大家的想象,像英伟达,Intel,AMD,Google,微软,亚马逊等占据巨大数据资源加上先进半导体科技技术的公司绝对是关注的重点。像英伟达在近6个月上涨了接近83%,AMD也有39%的上涨。

笔者曾在去年有写过,在半导体的争端之下,各个大型的半导体公司将会有不俗的发展,而今年的赛道不仅仅只是半导体等硬件,或是软件端的竞争,AI人工智能也加入了战局,传统型思维很有可能在近年被打破,无论是生活还是投资也将可能面临大的变革,我们拭目以待。免责声明:GO Markets分析师或外部发言人提供的信息基于其独立分析或个人经验。所表达的观点或交易风格仅代表其个人;并不代表GO Markets的观点或立场。联系方式:墨尔本 03 8658 0603悉尼 02 9188 0418中国地区(中文) 400 120 8537中国地区(英文) +248 4 671 903作者:Neo Yuan | GO Markets 分析师

热门话题五月以来,澳大利亚四大行已经陆续披露最新业绩报告。其中,NAB国民银行于5月4日率先公布半年报,股价单日下挫超6%,拖累银行板块。ANZ澳新银行、WBC西太银行紧随其后公布半年报,而CBA联邦银行于本周5月9日发布季报。市场反应来看,银行股整体表现不佳,这主要是由于两大预期扰动:净息差增长见顶以及经济放缓。

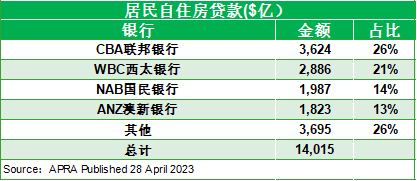

净息差已达峰值 澳联储加息尾期净息差NIM,即贷款收取的利息与为贷款支付的利息之间的差额,贷款是银行的核心业务,主要的盈利方式是通过融资与放贷之间的利息差赚取利润。在加息环境下一般认为净息差将提振银行净息差利润,然而由于澳洲房贷市场的激烈竞争,原本预期较高的息差利润效应受到侵蚀。根据澳大利亚审慎监管局4月28日发布的数据(截至3月),目前居民自住房贷款市场CBA占有最大份额,达26%,WBC西太银行21%紧随其后,NAB及ANZ各占14%及13%。

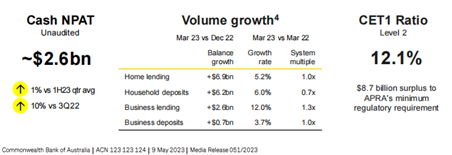

另一方面,澳洲物价数据拐头、澳联储4月曾暂停加息一次等信息来看,澳洲临近加息尾期,净息差不具备进一步扩大而为银行贡献利润增速的条件。加息环境下 衰退预期引发信贷风险在硅谷银行倒闭后,我们对澳大利亚银行体系持乐观态度。这是由于澳洲四大行的商业模式较为简单以传统银行业务的息差收入为主导,存款基础具备粘性,同时对全球风险资产的敞口较低且有相应利率对冲举措。加息环境下,尽管澳洲银行不像美国那样面临长期债券价值下跌的抛售侵扰,但信贷风险在经济衰退下引发市场担忧。尤其是加息对经济效应存在滞后性,经济一旦下行,居民存款下降、房贷需求下降、坏账及违约可能大幅提升。5月4日 NAB整体不达预期 股价单日下挫超6%NAB半年收入同比增长19.3%,现金收益增长17%,达40.7亿澳元,低于市场普遍预期的41.5亿澳元。净息差上升16个基点至1.77%,不达预期,且从今年一季度开始,净息差略有下降。一级资本充足率维持强劲,较22财年上升70个基点至12.21%。宣布中期股息为0.83澳元/股,22年年为0.73澳元/股,股息恢复疫情前水平(2019年中期股息0.83澳元VS 2020年中期股息0.3澳元),但这仍小幅低于市场预期。5月5日,ANZ澳新银行 股息略高于预期 净息差不及预期在截至3月31日的6个月里,NIM为1.75%,而分析师的预期为1.83%。公司持续经营业务的现金收益增长了12%,同样受到净息差和房贷业务需求增长的带动。净息差上升7个基点,至1.75%。一级资本充足率上升89个基点至13.2%。中期股息提高9.5%,至每股0.81澳元,小幅高于市场预期。管理层表示,接下来的六个月将更加艰难,由于零售银行业的激烈竞争。此外,澳新银行在四大行中对新西兰地区的敞口较大,因此新西兰加息市场可能会对ANZ的净息差形成一定支撑(本轮加息,目前新西兰加息500基点,对比澳洲加息375bp)。我们认为这也是财报后新西兰股价表现在四大行中表现较好的理由之一。5月8日 Westpac淡出住房贷款竞争,着眼商业贷款市场半年净利息收入增长10%,税后净利润增长22%至40.1亿澳元。净息差上升5个基点至1.96%。一级资本充足率上升95个基点至12.3%。中期股息上涨15%至每股70澳分。Westpac表示淡出住房贷款激烈竞争,着眼商业贷款市场。该举措虽然受到市场认可,但更为依赖于不确定性高的经济前景的商业贷款策略短期内无法对股价形成支撑。5月9日 CBA停止房贷市场竞争 预计经济增长放缓CBA国民银行三季度税后净利润26亿,同比上升10%。CET1一级资本充足率12.1%。但该季度的净利息盈利下降了2%,住房贷款增加了69亿美元,同比增长5.2%;商业贷款增长26亿美元,同比增长12.0%,一级资本充足率12.1%。净息差方面CBA季报中并未列明,但是指出净利息盈利的下降是由净息差下降拖累,参考:CBA最近一次披露的净息差NIM为2.1%。CBA宣布6月1日起不再对新房贷申请者提供现金返利,相比较继续争夺房贷市场转而关注公司长期盈利稳定性。

银行股投资价值从核心资本来看,四大行CET1均高于 APRA(澳大利亚审慎监管局)对四大银行CET1资本比率最少10.5%的基准要求,也就是说,四大行安全性及稳定性有所保障,均具备较高吸收亏损能力缓冲资本,以及抵御不利经济形势的能力。

今年以来银行股表现不佳,与ASX200指数对比,今年以来ASX200指数上涨4.4%,同期仅ANZ略微超越ASX200指数,涨幅达4.52%。同期CBA下跌3.53%,WBC下跌4.4%,NAB表现最差下跌超10%。

但是对于追求长期稳定股息分红的投资者来说,银行股仍然是不错的选择。四大行银行股平均股息率近6%,与银行储蓄相比,即使在加息环境下仍具备投资竞争力。免责声明:GO Markets分析师或外部发言人提供的信息基于其独立分析或个人经验。所表达的观点或交易风格仅代表其个人;并不代表GO Markets的观点或立场。联系方式:墨尔本 03 8658 0603悉尼 02 9188 0418中国地区(中文) 400 120 8537中国地区(英文) +248 4 671 903作者:Cecilia Chen | GO Markets 分析师