110多年来,美联储(美联储)一直故意与白宫和国会保持一定距离。

它是唯一一个不像大多数机构那样向任何单一政府部门报告的联邦机构,并且可以在不等待政治批准的情况下实施政策。

这些政策包括利率决定、调整货币供应、向银行提供紧急贷款、银行资本储备要求以及确定哪些金融机构需要加强监督。

美联储可以对所有这些关键经济决策以及更多决策独立采取行动。

但是为什么美国政府允许这样做呢?以及为什么几乎每个主要经济体都采用了类似的中央银行模式?

美联储独立的基础:1907年的恐慌

美联储是在1907年恐慌之后于1913年成立的,这是一场重大的金融危机。它导致各大银行倒闭,股市下跌近50%,全国各地的信贷市场冻结。

当时,美国没有中央权力机构在紧急情况下向银行系统注入流动性,也没有防止银行连续倒闭推翻整个经济的中央权力。

摩根大通亲自利用自己的财富精心策划了一次救助计划,凸显了美国金融体系已经变得多么脆弱。

随后的辩论表明,尽管美国显然需要中央银行,但客观地认为政客处于不利地位,无法管理该银行。

此前在中央银行方面的尝试失败了,部分原因是政治干预。总统和国会使用货币政策来实现短期政治目标,而不是长期经济稳定。

因此,决定成立一个负责做出所有重大经济决策的独立机构。从本质上讲,美联储之所以成立,是因为不能指望面临选举和公众压力的政客在长期经济需要时做出不受欢迎的决定。

美联储独立是如何运作的?

尽管美联储被设计成一个独立于政治影响力的自治机构,但它仍然存在 问责制 致美国政府(以及美国选民)。

总统负责任命美联储主席和联邦储备委员会七位理事长,但须经参议院确认。

每位州长的任期为14年,主席的任期为四年。州长的任期错开排列,以防止任何一个政府能够在一夜之间更换整个董事会。

除了这个 “主板” 之外,还有十二家地区性联邦储备银行在全国各地开展业务。他们的总裁由私营部门董事会任命,并由美联储七位理事批准。其中五位总统与七位州长一起在任何时候对利率进行投票。

这创造了一个分散的结构,在这个结构中,任何个人或政党都无法决定货币政策。改变美联储的方向需要来自不同政府的多名任命者达成共识。

美联储独立的理由:尼克松、伯恩斯和通货膨胀宿醉

保持美联储独立性的最有力论据来自尼克松在1970年代担任总统的时期。

尼克松向美联储主席亚瑟·伯恩斯施压,要求他在1972年大选前保持低利率。伯恩斯顺从了,尼克松以压倒性优势获胜。在接下来的十年中,失业率和通货膨胀率同时上升(通常称为 “滞胀”)。

到1970年代末,通货膨胀率超过13%,尼克松下台,是时候任命新的美联储主席了。

那位新任美联储主席是保罗·沃尔克。尽管公众和政治压力要求降低利率和降低失业率,但他还是将利率提高到19%以上,试图打破通货膨胀。

这一决定引发了残酷的衰退,失业率达到近11%。

但是到了1980年代中期,通货膨胀率已回落到个位数的低水平。

面对民意调查数字的暴跌,沃尔克坚定不移地站在非独立政客本来会倒退的地方。

现在,“沃尔克时代” 被视为中央银行为何需要独立的大师班。这种痛苦的药之所以奏效,是因为美联储能够承受政治反弹,而政治反弹本来会打破一个自主权较弱的机构。

其他中央银行是独立的吗?

几乎每个主要的发达经济体都有独立的中央银行。欧洲中央银行、日本银行、英格兰银行、加拿大银行和澳大利亚储备银行的运作自主权都与美联储类似,不受政府约束。

但是,也有发达国家脱离独立中央银行的例子。

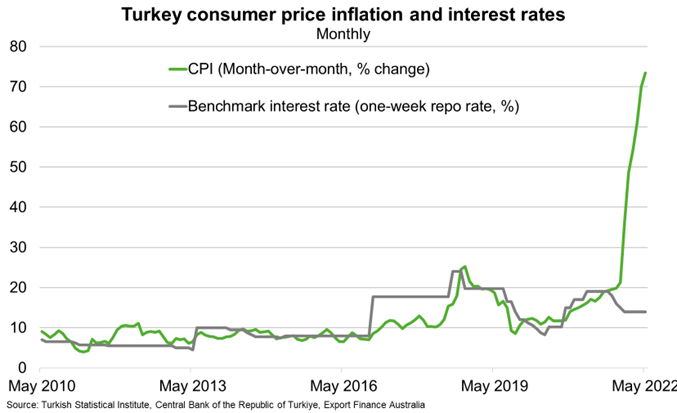

在土耳其,尽管通货膨胀率飙升至85%以上,但总统仍强迫其中央银行维持低利率。该决定为短期政治目标服务,同时摧毁了普通人的购买力。

服从于政治需求的货币政策加剧了阿根廷反复出现的经济危机。在政府宣布加强对委内瑞拉中央银行的控制之后,委内瑞拉的恶性通货膨胀加速了。

这种模式往往表明,政府对货币政策的控制越强,经济越倾向于不稳定和更高的通货膨胀。

独立中央银行可能并不完美,但从历史上看,它们的表现优于其他央行。

为什么市场关心美联储的独立性?

市场通常更喜欢可预测性,而独立的中央银行则做出更可预测的决策。

美联储官员经常概述他们计划如何调整政策以及他们首选的数据点是什么。

目前,消费者价格指数(CPI)、个人消费支出(PCE)指数、劳工统计局(BLS)月度就业报告和季度GDP报告构成了对未来利率走势的预期。

这种透明度和可预测性有助于企业规划投资,帮助银行设定贷款利率,帮助普通人规划重大财务决策。

当政治影响力渗透到这些决定中时,就会带来不确定性。利率可以根据选举考虑或政治偏好进行调整,而不是遵循基于公开发布的数据的可预测模式,这使得长期规划变得更加困难。

市场通过股价波动、潜在的债券收益率上升和货币价值的波动来对这种不确定性做出反应。

永恒的逻辑

美联储的独立性在于认识到,稳定的货币和可持续增长需要机构能够在经济基本面要求时做出不受欢迎的决定。

选举总是会给宽松的货币条件带来压力。通货膨胀总是会诱使决策者推迟痛苦的调整。而且政治日历永远不会与经济周期完全一致。

美联储独立的存在是为了应对这些永恒的紧张局势,这并不完美,但比历史上的政治控制要好。

这就是为什么这一在金融恐慌中形成并经过连续危机完善的原则仍然是现代经济运作的核心。这就是为什么关于中央银行独立性的争论,无论何时出现,都会触及民主国家如何维持长期繁荣的根本问题。

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs.