Last week was as consequential as advertised. The RBA hiked, the Fed held, and markets barely had time to process any of it before reports emerged that Israel had struck Iran's South Pars gas field.

The week ahead brings fewer central bank decisions, but it may be just as important for markets. Flash PMIs will offer the first broad read on whether the war is already showing up in business confidence. Australia's February CPI is the domestic data point that matters most for the RBA's next move. And the oil market remains the dominant macro variable.

Quick facts

- Brent crude spiked above $110 per barrel after Israel struck Iran's South Pars gas field for the first time.

- Flash PMIs for Australia, Japan, the eurozone, UK, and the US all land Tuesday.

- Australia's February CPI lands Wednesday, the first inflation read since the back-to-back RBA hikes.

Oil: From crisis to emergency

The oil situation deteriorated significantly last week. Brent crude has now surged roughly 80% since the war began on 28 February.

The 18 March strike on Iran's South Pars gas field was the first time upstream oil and gas infrastructure has been targeted.

Iran responded to the strike by threatening to target facilities across Saudi Arabia, the UAE and Qatar. If any of these threats are executed, the global oil shock would escalate from a supply disruption to a direct attack on the region's production capacity.

Analysts are now saying $150 Brent is achievable and $200 is not outside the realm of possibility. The 1970s Arab oil embargo resulted in a quadrupling of prices, and the current shock is already being described in those terms by senior energy executives.

For markets this week, oil is the dominant variable. Any signal of ceasefire, diplomatic progress or resumed Hormuz shipping could likely trigger a correction in oil prices. Any Iranian strike on Gulf infrastructure could send them higher.

Monitor

- Daily vessel transit numbers through the Strait of Hormuz.

- Iranian retaliation against Gulf infrastructure, a strike on Saudi or UAE facilities would be a major escalation.

- When and how American and European IEA reserves reach the market.

- Qatar's South Pars disruption is affecting the European LNG market.

- Trump statements that could cause intraday oil price movement.

Global Flash PMIs: The first read on an economy at war

Tuesday delivers the S&P Global flash PMI estimates for March across every major economy simultaneously.

This will be the first data set to capture how manufacturers and services firms are responding to $100+ oil, the Strait of Hormuz blockade, and the broader uncertainty created by the war in the Middle East.

The key question for each economy is whether the oil price surge and war uncertainty have dented business confidence, suppressed new orders or pushed input price indices to new multi-year highs.

Given that oil crossed $100 before the survey window closed for most economies, input cost readings could be significantly elevated.

Key dates

- S&P Global Flash Australia PMI: Tuesday 24 March, 9:00 am AEDT

- S&P Global Flash Japan PMI: Tuesday 24 March, 11:30 am AEDT

- HSBC Flash India PMI: Tuesday 24 March, 4:00 pm AEDT

- HCOB Flash France PMI: Tuesday 24 March, 7:15 pm AEDT

- HCOB Flash Germany PMI: Tuesday 24 March, 7:30 pm AEDT

- HCOB Flash Eurozone PMI: Tuesday 24 March, 8:00 pm AEDT

- S&P Global Flash UK PMI: Tuesday 24 March, 8:30 pm AEDT

- S&P Global Flash US PMI: Wednesday 25 March, 12:45 am AEDT

Monitor

- Input price components for any multi-year highs across manufacturing and services.

- Business confidence indices for how much the war shock has dented forward expectations.

- New orders as an indicator for future output; a sharp fall could signal demand destruction is underway.

- US composite PMI: already the weakest of major economies in February, another soft reading could raise growth alarm bells.

Hormuz crisis explained

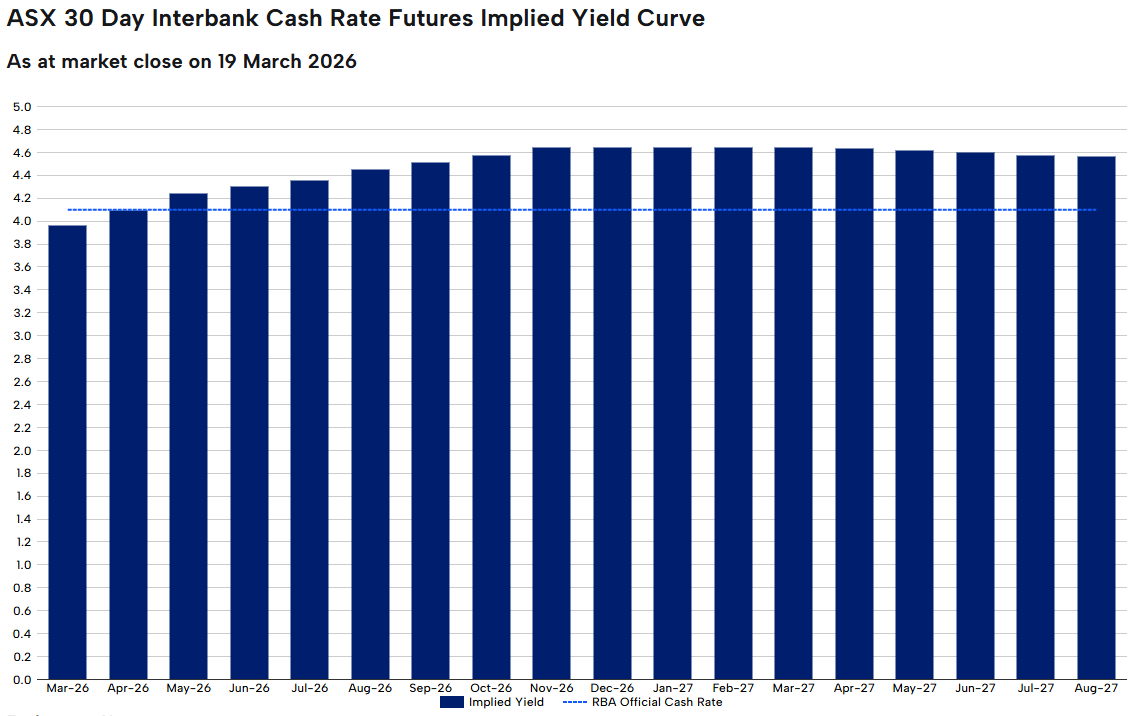

Australia: Is another hike coming?

The RBA hiked for the second meeting in a row on 17 March, lifting the cash rate to 4.10% in a narrow 5-4 vote.

Governor Bullock described it as a "very active discussion" where the direction of policy was not in question, only the timing.

This week will see the release of February's CPI as the first read to capture any of the oil shock. The trimmed mean, which strips out volatile items including fuel, will be the number the RBA watches most closely. A reading above 3.5% could cement the case for a May hike. A softer result could revive the argument for a pause.

ANZ and NAB have both stated expectations of a third hike in May, taking the cash rate to 4.35%.

Key dates

- ABS Consumer Price Index (CPI): Wednesday 25 March, 11:30 am AEDT

Monitor

- Trimmed mean inflation as the RBA's preferred measure.

- Fuel and energy components that could separate the oil shock from domestic price pressure.

- Housing and services inflation as sticky components driving the RBA's long-run concern.

Ready to trade beyond the majors?

Open an account · Log in

Reportingdates and release times are based on company investor relations calendars whereconfirmed. Where dates or times are not marked confirmed, they are GO Marketsestimates. Consensus EPS, revenue and analyst-range data are sourced fromBloomberg and Earnings Whispers, as at 09 July 2026 (AEST). Company guidance,backlog and operating metrics are sourced from the latest company filings orresults presentations, unless stated otherwise. Any scenario analysis reflectsGO Markets analysis. Figures and schedules may change without notice.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here.

Any references to Australian or international shares, sectors, indices, ETFs, crypto-related stocks or other instruments are provided for market commentary and watchlist purposes only and do not constitute a recommendation, offer or solicitation to buy, sell or hold any financial product or adopt any investment strategy. International markets may involve additional risks, including currency fluctuations, regulatory differences, market structure differences, reduced liquidity and higher volatility. Company-specific, sector-specific and macroeconomic risks may also affect performance.

Commentary on geopolitical developments, economic data, central bank decisions, earnings, policy changes and other global or financial market events is based on information available at the time of publication and may change without notice. Such events can lead to sudden market moves, price gaps, reduced liquidity, wider spreads and increased volatility, particularly in leveraged products such as CFDs. Forward-looking statements, expectations and scenario analysis are inherently uncertain and should not be relied on as guarantees of future market behaviour or outcomes.