热门话题

中美角逐已经从百亿爆仓的金融市场,递延到汇率市场和石油市场中。而下一个主战场,就是石油。石油是国家战略物资。有一本书,叫做《大国的崩溃,苏联解体的台前幕后》。书中解读了,石油如何影响苏联经济,并最终造成苏联产业结构失衡,在石油价格暴涨暴跌后,国家破产,最终解散。而石油核心的出口国,包括伊朗、伊拉克,都是国际政治的焦点,也是中美俄罗斯多国争夺的核心外交战略资源。随着疫情逐步缓解,经济恢复预期增强,石油价格也逐渐回升。目前,复活节Easter holiday刚刚结束,悉尼的Easter show 每天限额6万张票,都是提前一周就售完。足以见到实体经济已经开始恢复。而全球GDP增速和石油消费量增速基本保持一致。所以,世界货币基金组织预计今年的国际GDP增速提高至5%以上,意味着短期石油消耗需求会增加。

近期导致石油价格快速上升的几点:1. 航线受阻。多条航线拥挤,受到沉船等因素影响,几条航线比预期要拥堵。有点类似发生了车祸造成的堵车现象。2. 另外,可用的油轮数量减少。运输成本上升。受中美摩擦影响,很多轮船在海关停靠,或无法进关,或无法清关,造成航运能力下降,石油价格上升。3. 通胀预期走强。货币超发对于商品,尤其是原料价格和农业工业等上游价格影响较大。物价上涨也是必然。4. 减产协议的生效,对于石油价格有着直接的短期提振。我们看下面的图:

自从疫情以来,中东OPEC各国和主要石油生产商,多次谈判减产。而当进入2021年,石油价格回升至60美金上方之后,开始增产。从今年5月开始,沙特逐步取消100万桶每日的减产规模,将直接导致供给增加。

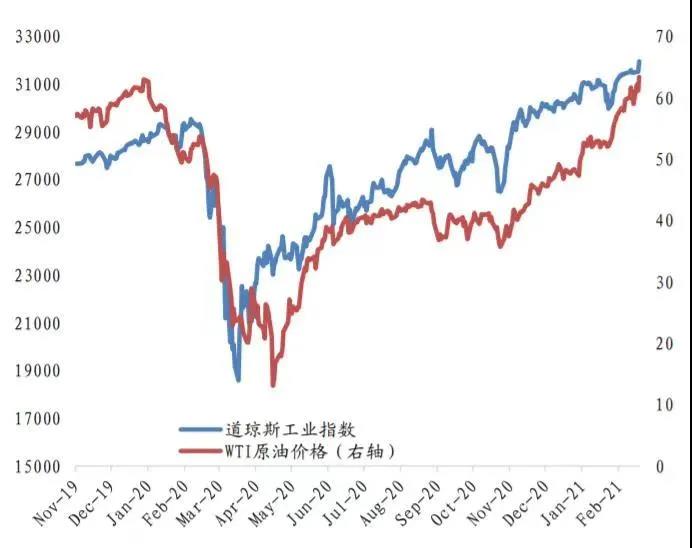

另外,主要石油生产商伊朗,受到美国经济制裁,目前伊朗核协定短期无法得到有效解决,所以伊朗把石油出口给中国。而中国不惧怕美国,接受伊朗原油。因此,世界上主要的两大石油需求国,中国和印度,前者进口伊朗原油,降低了国际原油市场的需求。后者疫情控制很差,短期国内石油需求急剧下滑。这两个石油需求国家,对于流动的美国和英国计价的石油需求都大幅度下降。石油生产企业的平均成本价格在35美金左右。因此,石油价格最低的容忍区间应该是35-60美金浮动。而中东大部分国家的财政收支平衡实在70美金左右。因此,当石油价格超过70美金上方,对于竞争者来讲,我们做生意的时候,如果是和竞争对手出现严重矛盾,那么我们最简单粗暴的方式,就是增产降价。因此,一旦国家盈亏为正数,就会出现大量的增产,最终石油价格暴跌。对于我们有股票的投资者来讲,美国道琼斯指数ws30和石油价格呈现很强的关联性。所以我们可以考虑做空石油价格,来对冲保护我们的股票投资组合。

免责声明:GO Markets分析师或外部发言人提供的信息基于其独立分析或个人经验。所表达的观点或交易风格仅代表其个人;并不代表GO Markets的观点或立场。联系方式:墨尔本 03 8658 0603悉尼 02 9188 0418

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. 免责声明:文章来自 GO Markets 分析师和参与者,基于他们的独立分析或个人经验。表达的观点、意见或交易风格仅代表作者个人,不代表 GO Markets 立场。建议,(如有),具有“普遍”性,并非基于您的个人目标、财务状况或需求。在根据建议采取行动之前,请考虑该建议(如有)对您的目标、财务状况和需求的适用程度。如果建议与购买特定金融产品有关,您应该在做出任何决定之前了解并考虑该产品的产品披露声明 (PDS) 和金融服务指南 (FSG)。

.jpg)